How much is home insurance?

12/03/2025

How much is home insurance? Find out the average cost of UK home insurance for your region and property type, along with other helpful home insurance statistics for 2025.

Find data on UK home insurance costs in 2025

- The average cost of home insurance

- Regional home insurance costs

- Home insurance price differences across property types

- Regional residential burglary incidents vs home insurance costs

- Regional crime rates vs national average

- Council tax increases

- Regional noise nuisance statistics

- Regional average house prices

Home Insurance Price Index 2025

The average home insurance cost in the UK is £274.17 going into 2025.

Like other major insurance products, home insurance premiums have faced a steep increase in recent years. With the cost of insuring a home in England up an average of 60% since the beginning of 2023.

This is down to a combination of factors including inflation, rising labour and repair costs, and an unusually high number of claims paid out by UK insurers. All these factors have pushed up the cost of home insurance for the average UK homeowner.

How much does home insurance cost?

The price of your home insurance will vary depending on the region you live in and the type of property you own.

Factors such as local repair and labour costs, crime rates, flooding, and the overall number of claims for your region will also impact how much you pay on your cover.

Quotezone home insurance data reveals the average cost broken down by region.

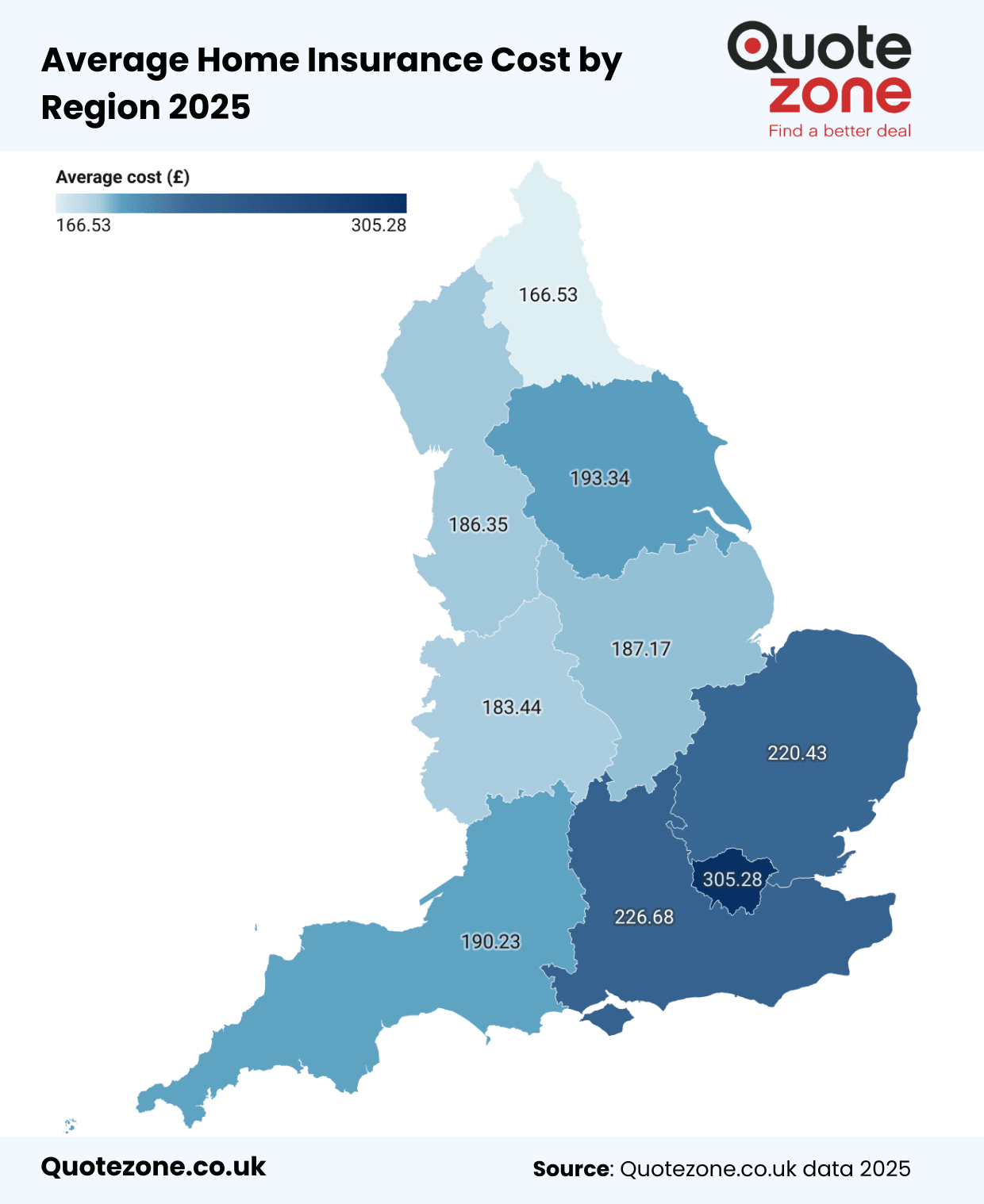

Regional home insurance costs

| Regions | Average Annual Home Insurance Cost Q1 2023 | Average Annual Home Insurance Cost Q1 2024 | Average Annual Home Insurance Cost Q4 2024 |

|---|---|---|---|

| London | £181.15 | £289.38 | £305.28 |

| South East | £133.94 | £197.23 | £226.68 |

| East of England | £136.14 | £192.68 | £220.43 |

| South West | £115.56 | £166.14 | £190.23 |

| West Midlands | £119.63 | £163.48 | £183.44 |

| East Midlands | £122.63 | £166.43 | £187.17 |

| North West | £118.51 | £168.73 | £186.35 |

| Yorkshire and The Humber | £127.92 | £170.69 | £193.34 |

| North East | £108.55 | £158.12 | £166.53 |

Will the cost of home insurance fall in 2025?

The average cost of home insurance has risen in the last year for all property types.

This was originally in line with premium increases for insurance products across the board. However, while the average cost of car insurance has started to fall again in 2025, home insurance costs are still rising.

London homeowners saw a 69% increase in their home insurance premiums between Q1 2023 and Q4 2024. Meanwhile, those living in the North East felt a 53% increase in their home insurance premiums.

It is hard to say for sure if home insurance premiums will continue to rise, or fall throughout 2025. Some of the key determining factors include the rate of inflation and the volume of claims received by insurers, as well as the associated costs of these claims.

What is causing the increase in home insurance premiums?

There have been several factors impacting the price of home insurance premiums in the last year. The main drivers of this include bad weather and natural disaster events, along with increased repair and service costs.

According to the ABI, UK insurers paid out £352 million within 12 months due to home insurance claims resulting from natural disaster damages. And with as many as 12 named storms happening in a 12-month period between 2023 and 2024, these expenses look set to continue.

The cost of repairs has also been increasing as a result of the cost of living crisis, forcing insurers to pay out more on average for each home insurance claim. This coupled with the larger volume of claims has forced insurers to raise the cost of their premiums to compensate for the increased payouts made in the last year.

Does the size of a property affect the price of home insurance?

Yes. Generally speaking, the more bedrooms a property has, the higher the price of your home insurance policy.

So, the average home insurance cost for a 3 bedroom property will differ from the average cost for a 4 bedroom property, due to the extra value added by additional rooms.

The building’s value and the average value of the home’s contents will both contribute. This is why fully detached homes are typically more expensive to insure than an apartment.

Here is a breakdown of the average home insurance prices in the UK for different property types from Q1 2023 – Q4 2024.

Home insurance price differences across property types

| UK Property Type | Average Annual Home Insurance Cost Q1 2023 | Average Annual Home Insurance Cost Q1 2024 | Average Annual Home Insurance Cost Q4 2024 |

|---|---|---|---|

| Detached | £270.67 | £394.86 | £308.66 |

| Semi-Detached | £180.55 | £255.09 | £265.16 |

| Terraced | £166.91 | £227.88 | £259.38 |

| Apartment | £66.39 | £80.39 | £160.07 |

How much is home insurance in your location?

Your location gives insurers a lot of information about the risk of insuring your home. This means that insurers can use regional home insurance data to determine the likelihood of you claiming on your home insurance policy.

One of the major factors that insurers will examine when looking at your property’s location will be the regional crime rate. The number of burglaries in your area will be of particular interest as these can result in costly home and contents insurance claims.

Regional residential burglary incidents

| Regions | Residential Burglary Incidents | Average Annual Home Insurance Cost Q1 2024 |

|---|---|---|

| London | 38,040 | £289.38 |

| Yorkshire and The Humber | 25,206 | £170.69 |

| North West | 24,489 | £168.73 |

| West Midlands | 22,894 | £163.48 |

| South East | 20,149 | £197.23 |

| East of England | 14,187 | £192.68 |

| East Midlands | 13,847 | £166.43 |

| South West | 11,001 | £166.14 |

| North East | 10,716 | £158.12 |

Whilst burglary rates are not the only factor that insurers consider when looking at your property’s location, it is a direct factor that is used in calculating your premiums.

Other risks such as how prone the area is to flooding, the cost of labour and repairs in your local area, as well as the value of your property will all also be used when calculating your premiums.

Regional crime rates

Crime rates can have a huge impact on the cost of insuring a property in a given area. Not only can it impact the cost of insuring your home, but it can also be an important consideration when it comes time to purchase a property.

| Regions | Total Crimes | Crime Rate | Crime Rate Difference from England average |

|---|---|---|---|

| London | 933,287 | 87 | 2.5% safer |

| South East | 724,258 | 67 | 24% safer |

| East of England | 460,782 | 70 | 22% safer |

| South West | 399,816 | 56 | 37% safer |

| West Midlands | 560,608 | 69 | 22% safer |

| East Midlands | 413,572 | 79 | 11% safer |

| North West | 753,266 | 47 | 47% safer |

| Yorkshire and The Humber | 611,655 | 90 | 1.3% more dangerous |

| North East | 293,004 | 76 | 14% safer |

Factors to consider when purchasing a UK property

Council tax increase

Council tax is one of several cost increases UK homeowners have faced in recent years. 2025 council tax increases are a repeat of previous years in many areas. And this can be off-putting for potential home buyers in certain areas, as council tax can be a considerable additional cost.

Find out how much council tax has increased across 13 councils in England.

Noise nuisance statistics

Noise nuisance or noise pollution can lead to many sleepless nights and potential arguments with neighbours and your local council. When it comes to purchasing a home, potential noise pollution is something homeowners should consider.

Whilst noise pollution won’t impact your home insurance premiums directly, it can still have an influence. Some soundproofing installations in your home, such as further insulation, chimney caps and window frame replacements, can all add value to your property, which may potentially increase your home insurance costs.

Here are the regions broken down by the number of noise nuisance complaints.

| Regions | People highly annoyed by road noise (per 100k people) | People highly sleep disturbed by road noise (per 100k people) |

|---|---|---|

| London | 116 | 101 |

| South East | 80 | 66 |

| East of England | 54 | 37 |

| South West | 53 | 41 |

| West Midlands | 78 | 64 |

| East Midlands | 55 | 41 |

| North West | 99 | 79 |

| Yorkshire and The Humber | 69 | 55 |

| North East | 55 | 36 |

Regional house prices

This may seem like an obvious thing to consider, but the average cost of a property varies across the UK. Whilst London has traditionally been the most expensive location for purchasing a home, it is also the region that experienced the greatest decline in average property price.

| Regions | Average House Price | House Price Monthly change | House Price Annual change |

|---|---|---|---|

| London | £502,690 | -0.70% | -4.80% |

| South East | £373,018 | 1.10% | -2.10% |

| East of England | £339,144 | 1.70% | -1.60% |

| South West | £316,834 | 0.50% | -0.40% |

| West Midlands | £242,429 | -1.20% | -2.90% |

| East Midlands | £241,950 | 1.40% | -0.40% |

| North West | £213,890 | -0.20% | 1.40% |

| Yorkshire and The Humber | £204,754 | 0.90% | 0.20% |

| North East | £160,406 | 3.20% | 2.90% |

Last Updated: 12 March 2025

Read time: 8 minutes

Written by: Lauren McAfee

Insurance Writer and Editor

Reviewed by: Katie Gawley

Written in line with our Editorial Guidelines

House swapping – are you actually insured?

Home exchange, sometimes called house swapping, is becoming an increasingly popular way to travel in the UK while reducing accommodation…

Property red flags that could cost buyers over £50k

Homebuyers are being warned not to overlook property red flags which could result in unexpected costs of up to £53,000. …

How to reduce your energy bills

With winter energy bills expected to rise, experts from Quotezone provide simple and effective tips for reducing your energy bills…

Keep costs down by spotting common boiler red flags

Households are being urged to conduct simple boiler checks before the UK is hit with freezing temperatures, to ensure homes…

Over 100,000 burglaries a year as autumn raises alarm

Homeowners are being urged to step up security measures as data reveals more than 100,000 burglaries took place in the…

Rat threat to UK properties this winter

UK homeowners are being warned that rat infestations could slash property prices, derail house sales, and even leave them without…

References

https://www.gov.uk/government/news/uk-house-price-index-for-january-2024

https://www.abi.org.uk/news/news-articles/2024/2/the-cost-of-home-insurance-rises-as-insurers-support-

https://www.bbc.com/news/uk-politics-55765504

Road traffic noise DALY rates (per 100,000 people) by English regions (2018).

https://crimerate.co.uk/england

UK House Price Index summary: February 2024 – GOV.UK (www.gov.uk)

https://www.statista.com/statistics/1552429/number-of-named-storms-uk/

This article is intended as generic information only and is not intended to apply to anybody’s specific circumstances, demands or needs. The views expressed are not intended to provide any financial service or to give any recommendation or advice. Products and services are only mentioned for illustrative rather than promotional purposes.