Ignoring service lights could leave drivers uninsured

A simple dashboard warning light could end up costing drivers far more than they realise, according to motoring experts. Research…

Don’t have your registration number? No problem, click here.

Car insurance is a legal requirement for anyone driving on UK roads. Under the Road Traffic Act 1988, you must hold at least third party cover before driving or keeping a vehicle on public roads. Failing to insure your vehicle can result in a £300 fixed penalty, six penalty points, and in serious cases your vehicle may be seized and destroyed.

There are three main levels of cover: third party only (the legal minimum), third party fire and theft, and fully comprehensive. The right choice depends on your vehicle, driving history and budget. According to the Association of British Insurers, around 30 million motor insurance policies are active in the UK at any time. Quotezone compares car insurance quotes from over 130 FCA-regulated UK providers, helping you find the right cover at a competitive price in minutes.

When you take out a policy, you pay a premium to an insurer who agrees to cover the cost of certain events such as accidents, theft, or damage to other vehicles. If you need to make a claim, you pay an excess (a fixed amount you contribute) and your insurer covers the rest up to your policy limit.

Premiums are calculated based on several factors including your age, driving experience, claims history, the vehicle you drive, where you live, and the level of cover you choose. Insurers use data from the Motor Insurance Database, managed by the Motor Insurers’ Bureau, to verify that all UK vehicles are covered.

You can buy car insurance directly from an insurer, through a broker, or by using a comparison site like Quotezone. Using a car insurance comparison site is the most effective way to find competitive cover, as prices for identical policies can vary significantly between insurers.

There are three levels of car insurance available in the UK. Fully comprehensive is not always the most expensive — drivers who choose comprehensive cover tend to make fewer claims, so insurers often price it more competitively than third party only. Always compare all three levels when you get quotes.

| What’s covered | Third Party Only | Third Party Fire & Theft | Fully Comprehensive |

|---|---|---|---|

| Damage to other vehicles | ✓ | ✓ | ✓ |

| Injury to other people | ✓ | ✓ | ✓ |

| Damage to your car in an accident | ✗ | ✗ | ✓ |

| Fire damage to your car | ✗ | ✓ | ✓ |

| Theft of your car | ✗ | ✓ | ✓ |

| Windscreen cover | ✗ | ✗ | Often included |

| Personal accident cover | ✗ | ✗ | Often included |

| Legal minimum to drive in UK | ✓ | ✓ | ✓ |

Your premium comes down to one thing: how likely you are to make a claim, and how much that claim might cost. Insurers assess this differently, which is why two people with the same car can get very different quotes.

Age is one of the biggest factors. Drivers under 25 pay more because statistically they are more likely to be involved in an accident — this isn’t personal, it’s just how the data falls. Premiums typically drop as you gain experience and build up a no-claims discount, which after five or more years can reduce your premium by 60–75%.

The car itself matters too. Every vehicle is assigned to one of 50 insurance groups based on repair costs, performance and safety features. Higher group means higher premium, as a rule.

Where you live has more impact than most people realise. Urban postcodes — particularly in London and Birmingham — attract higher premiums due to greater rates of theft and accident claims. Your occupation plays a similar role, with some jobs statistically linked to higher risk than others.

One thing worth knowing: fully comprehensive cover is not always more expensive than third party only. Drivers who opt for comprehensive cover tend to be lower risk, so insurers price it accordingly. It is always worth comparing all three levels before assuming the cheapest option is third party.

Quotezone searches over 130 UK providers to help you find cheap car insurance that suits your specific circumstances.

For most drivers, the no-claims discount is often the single biggest factor affecting their premium. Every claim-free year adds to it. After five or more years, it can reduce your premium by 60–75% compared to what you’d pay with no discount history. That’s not a small difference — and it’s one of the most reliable ways to secure cheap car insurance at renewal without changing your cover.

The discount is yours, not the car’s. Switch insurer, change vehicle, it comes with you — you’ll just need proof from your previous provider. If you run two cars on separate policies, each one builds its own NCD independently, which is worth knowing.

One thing that catches people out: NCD protection doesn’t freeze your premium after a claim. It protects the discount itself, but insurers can still adjust your base rate. So after a claim, you might keep your five-year discount but still see your renewal price go up. Whether the protection add-on is worth paying for depends on how big your discount is and what the add-on costs. It’s worth doing the maths rather than assuming it’s always a good deal.

We’ll quickly find your car’s make and model using your registration number. You’ll need to know its estimated value, security features, and your annual mileage.

Your name, age, address – plus your occupation, driving history and previous claims on your policy.

Choose between fully comprehensive cover, third-party, fire and theft, or third-party only. You’ll also be asked how you use your car and what level of excess you prefer.

We search over 130 car insurance providers to save you hassle and money

Compare Car Insurance

We search over 130 car insurance providers to save you hassle and money

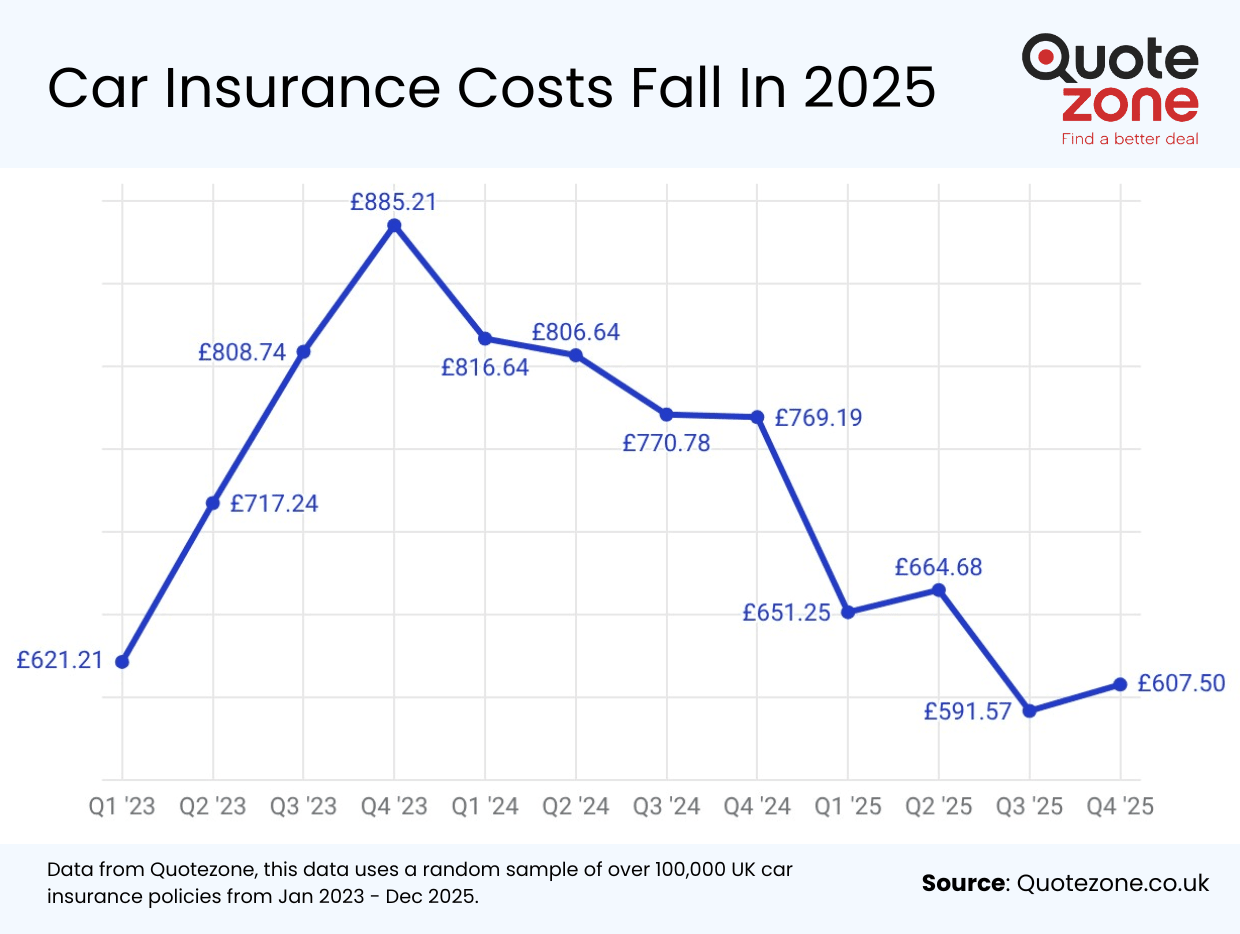

In 2025, car insurance cost £591.63 for the average UK motorist, according to Quotezone market data. When it comes to individual costs, it will depend on how likely you are to make a claim on your insurance policy. Insurers use the details you provide when you get a quote to judge how risky you are to insure.

Some of the biggest risk indicators are your age and location. The average insurance costs shown below display just what a massive difference these can make to the price of your insurance.

The right type of car insurance depends on how you use your car, who drives it, and what you can afford to lose if something goes wrong. The policies below cover the most common situations — click any of them to find out more and compare quotes.

Car insurance premiums peaked in late 2023, driven by a surge in claims and the rising cost of repairs. Insurers had been absorbing years of inflation in parts and labour, and eventually passed those costs on to drivers. As a result, motor insurance costs in the UK reached a 5 year high at the time. However, our insurance cost data shows that premiums were continuing to fall in 2025 until the last quarter, when there was a slight increase, but are still 21% cheaper than this time last year. A quick car insurance comparison on Quotezone can show exactly how these lower prices translate to your own premium.

Finding cheap car insurance in the UK has become more difficult as premiums have risen in recent years. With motor insurance costs spiking in previous years, it’s more important than ever to know how to find cheap car insurance.

If you can pay upfront, do. Monthly payments are essentially a loan – most insurers charge the equivalent of 20–30% APR in interest, which adds a noticeable amount to the total cost over the year. If paying in full isn’t realistic, it’s still worth comparing the annual total rather than just the monthly figure, as interest rates vary significantly between insurers.

Parking on a private driveway rather than a public road can save you up to £140 on your premium, according to Quotezone data. Upgrading security with an engine immobiliser or GPS tracker can also bring the price down – insurers price risk, and a harder-to-steal car is a lower risk.

Your current insurer won’t automatically offer you their best rate at renewal. The Association of British Insurers recommends comparing quotes before every renewal rather than accepting the first price you receive. Prices for identical cover can vary by hundreds of pounds between providers – comparing on Quotezone takes a few minutes and shows you what the full market will charge.

Every claim-free year adds to your no-claims discount. After five or more years it can reduce your premium by 60–75%. For minor incidents where the repair cost is close to your excess, it’s often cheaper to pay out of pocket and protect the discount than to claim and see your premium rise at renewal.

Adding a more experienced driver to your policy can bring the premium down if they genuinely share the car. One thing to be clear on: the main driver listed must be whoever actually drives it most. Adding someone purely to cut the price – when they rarely or never use the car – is fronting, which is fraud and can void your cover entirely.

Black box or telematics policies price your cover based on how you actually drive rather than statistical averages for your age group. For careful or low-mileage drivers – particularly those aged 17 to 24 – this can be considerably cheaper than a standard policy. If you drive mainly at lower-risk times and cover fewer miles than average, it’s worth getting a telematics quote alongside your standard comparison.

Agreeing to pay more if you claim reduces the insurer’s exposure, which typically brings the premium down. Before you increase it, check what your compulsory excess already is – the two are added together, so make sure the combined total is an amount you could comfortably pay if you needed to make a claim.

Every car in the UK sits in one of 50 insurance groups, set by the Association of British Insurers Group Rating Panel. Group 1 is the cheapest, group 50 the most expensive – a group 1 car can cost half as much to insure as a group 20 equivalent. If you are buying a new car and running costs matter, it is worth checking the group before you commit.

Prices tend to be sharpest 20 to 30 days before your renewal date. Leaving it until the day your policy expires signals urgency, and insurers price accordingly – last-minute buyers typically pay more. Quotezone sends renewal reminders at the right time so you don’t miss the window.

Most standard policies can be extended with optional add-ons. Some are worth having for most drivers — others are only relevant in specific situations. Here’s what’s available and when each one makes sense.

Car breakdown cover offers roadside assistance to help get you back on the road when your car breaks down.

When your windscreen is cracked or chipped, windscreen cover will pay to repair or replace the glass.

Excess protection cover lets you claim back any voluntary or involuntary excess you’ve paid when claiming on your car policy.

Driving other cars, or DOC insurance covers you for driving other people’s cars, as long as you have their permission.

A long no-claims history can go a long way towards getting more competitive insurance quotes for your car. No claims bonus protection means you can keep these savings even if you make a claim.

European car insurance provides comprehensive coverage when you drive abroad. It means you have protection when driving in EU countries, including Ireland.

Being familiar with the basics of making a claim before an accident can help make an unpleasant situation less stressful. Knowing what to do after a car accident means you can stay calm, and get the information and evidence you need for a smooth and quick resolution.

Regardless of if the accident was your fault, or you were hit by another driver, contact your own insurer. Let them know the date, time and location of the incident. and any other parties involved.

You will need to share your insurance policy number and any documents that support your claim. This can be a police report, photos, dash cam footage, or contacts for witnesses.

Your insurers will investigate the claim and its evidence and will authorise compensation or repairs through a chosen garage if the claim is approved.

When the claim is settled you will be reimbursed for the repairs to your car. How long it will take to settle your insurance claim will vary depending on the insurer and the complexity of the claim.

You should expect your premiums to decrease as you get older and more experienced, however as you reach retirement age, you may again see rises in your premiums. It is useful to know how your age relates to pricing of car insurance so you can budget your car insurance policy. You can compare quotes by age, to get you the right cover for the best price.

Quotezone compares policies from over 130 FCA-regulated UK providers, including major names like Admiral, AXA, Churchill, Direct Line, Hastings Direct and RAC. The panel also includes a range of smaller and specialist insurers who may offer more competitive rates for certain drivers and vehicles, including those with convictions, modified cars, and imported vehicles.

The reason panel size matters is that car insurance pricing is personal. The insurer that’s cheapest for a 45-year-old in rural Yorkshire may be one of the most expensive for a 23-year-old in Birmingham. Searching across a wide panel means you’re not relying on one provider’s view of your risk — you’re seeing the actual range of what the market is likely to charge you. It’s one of the most effective ways to find cheap car insurance, as the insurer offering the lowest price varies significantly depending on your individual risk profile.

Quotezone is free to use, FCA-regulated, and has no ownership ties to any of the insurers we compare. If you want to explore specific providers, the full list is here.

For more advice on car insurance, see our full collection of car insurance guides.

Reviewed by: Greg Wilson

Founder & Insurance Expert

Written by: Katie Gawley

Insurance Content Writer

Fact-checked by: Quotezone Editorial Team

This content follows our Editorial Guidelines

Last Updated: 1 April 2026

Great choice . Multiple Quotes provided. Thank you

Suryakant

“”

No hassle quote.

kevin

en, en

4.86/5 from 1224 customer reviews

A simple dashboard warning light could end up costing drivers far more than they realise, according to motoring experts. Research…

No, you cannot backdate a car insurance policy in the UK. Every motor insurance policy starts from the date and…

UK drivers are backing the government’s proposed road safety strategy, as new research reveals strong public support for stricter rules…

Avoid costly wet-weather driving mistakes that could cost up to £5,000, with essential tips from Quotezone to keep UK drivers…

Confused about auto-renewal on your car insurance? Our insurance experts share everything you need to know about auto renewals and…

UK motorists are being shown how simple adjustments could help them save hundreds on their car insurance in 2026.

Compare quotes from over 130 car insurance companies

Our car cover comparison services increases your chance of finding a great deal by comparing 130+ quotes side-by-side.

Buy your car policy online or over the phone

Sign up online or over the phone, and choose from monthly or annual payment options.

Save on your insurance

One short form is all it takes to compare cheap insurance policies from over 130 providers.

Over 4 million users

Over 4 million people save money with us each year.

Secure & Encrypted

We guarantee your confidence when shopping online by following the latest internet security standards.

Independent and unbiased service

We aren’t owned by or have any investment from any insurance company.

*51% of consumers could save £518.14 on their Car Insurance. The saving was calculated by comparing the cheapest price found with the average of the next four cheapest prices quoted by insurance providers on Seopa Ltd’s insurance comparison website. This is based on representative cost savings from June 2025 data. The savings you could achieve are dependent on your individual circumstances and how you selected your current insurance supplier.